In a February interview with New York Magazine, Gary Gensler, chairman of the United States Securities and Exchange Commission, said that just about every crypto transaction, with the exception of Bitcoin spot transactions and buying or selling things with cryptocurrency, falls within the jurisdiction of the SEC.

In the interview, when discussing what types of crypto transactions should be regulated as securities, Gensler didn’t mince words. “Everything other than Bitcoin. You can find a website, you can find a group of entrepreneurs, they might set up their legal entities in a tax haven offshore, they might have a foundation, they might lawyer it up to try to arbitrage and make it hard jurisdictionally or so forth,” Gensler said.

Gensler continued, “They might drop their tokens overseas at first and contend or pretend that it’s going to take six months before they come back to the U.S., but at the core, these tokens are securities because there’s a group in the middle and the public is anticipating profits based on that group.”

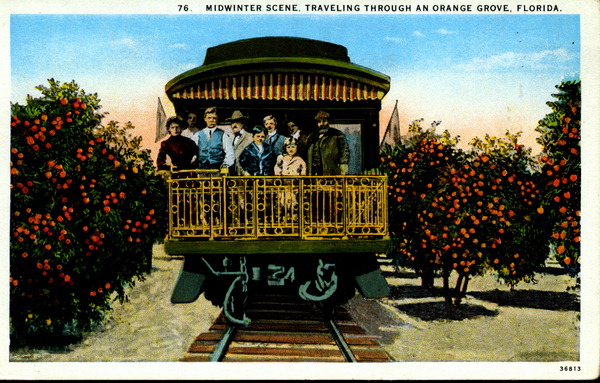

Gensler contends that the SEC’s jurisdiction over most cryptocurrencies is based on a 1946 Supreme Court ruling in the case SEC v. W.J. Howey Co. According to Investopedia, the W.J. Howey Co. sold citrus groves to Florida buyers. Those buyers would lease the groves back to the company. The company cultivated the trees and sold the oranges on behalf of the Florida buyers. Both would share in the profits. W.J. Howey Co. subsequently failed to register with the SEC, arguing that its transactions were not investment contracts.

(State Library and Archives of Florida, Public domain, via Wikimedia Commons)

W.J. Howey Co. lost the case when the court ruled that the leaseback arrangements were investment contracts, thus establishing the Howey test wherein four criteria are used to determine whether something constitutes an investment contract: An investment of money, in a common enterprise, with the expectation of profit, to be derived from the efforts of others.